The hottest investment story of the decade is also becoming one of its biggest financial questions.Artificial intelligence has shifted from a futuristic promise to an economic obsession. Tech companies race to build ever‑larger models, governments compete to secure semiconductor supply chains, investors pour billions into AI infrastructure, and markets reward firms that merely hint at an AI strategy with eye‑catching valuations.It’s a familiar script. Which is perhaps why the world’s “central bank for central banks” has asked an uncomfortable question: are we witnessing the early stages of another dot‑com moment?Not because AI lacks transformative potential — far from it — but because history shows revolutionary technologies often come with speculative excess. The BIS writes, “Historical episodes of investment booms offer instructive parallels. The canal mania of the 1830s, the British railway mania of the 1840s, the electrification exuberance of the late 1920s and the dot‑com boom of the late 1990s all shared one common trait: a genuine technological breakthrough that attracted capital in excess of what commercial returns could ultimately justify.” Such moments produce extraordinary optimism; sometimes they create lasting wealth, sometimes they end in painful bubbles.The BIS’s Annual Economic Report stops short of predicting an AI crash. Instead, it gives a more measured warning: don’t confuse genuine technological progress with the assumption that every dollar poured into AI today will yield sustainable returns tomorrow. It named the sustainability of the AI build‑out as one of four pressure points threatening the global economy, alongside returning inflation, strained public finances, and growing financial vulnerabilities.As the report puts it, “the sustainability of AI‑related investments deserves close attention.” That caution lies at the heart of the debate.

A quick rewind: what was the dot‑com bubble?

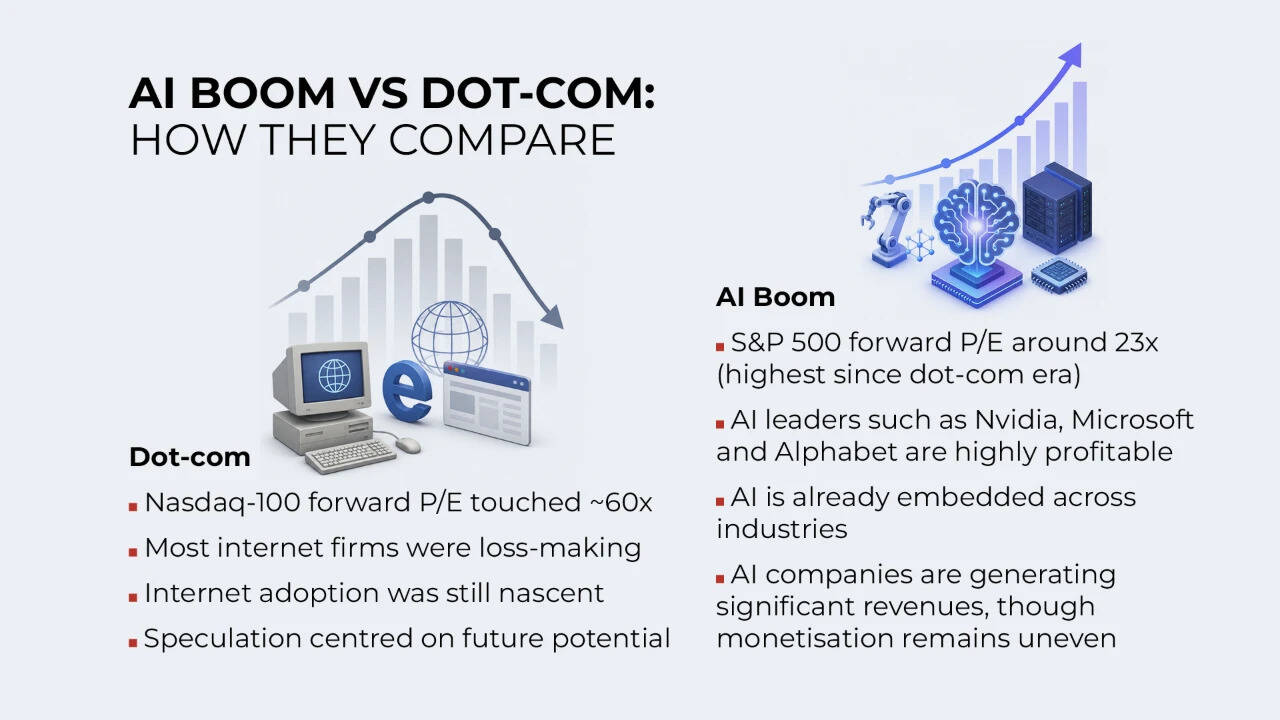

To see why the comparison has resurfaced, revisit a famous episode in financial history.In the late 1990s the commercial internet promised to transform business and daily life. Investors rushed to back internet companies, many of which had little more than ambitious plans, minimal revenues and no clear path to profitability.Share prices rose simply because a company’s name ended with “. com.” Traditional measures such as earnings or cash flow were often ignored in favour of speculative expectations about future growth. Venture capital flooded the sector, initial public offerings multiplied, and market enthusiasm became self‑reinforcing.The optimism was not entirely misplaced. The internet did transform the global economy. Companies such as Amazon survived and eventually reshaped commerce. But many others disappeared almost as quickly as they had emerged.When interest rates rose and investors began questioning valuations, the bubble burst. Between 2000 and 2002 technology stocks lost trillions in market value, thousands of companies failed and investment dried up. The lesson: the internet was real, but markets had dramatically overestimated how quickly profits would follow innovation.That distinction is precisely why today’s AI boom deserves scrutiny.According to Vishwa Kiran, chief technology officer at Skillmine Technology Consulting, history appears to be rhyming. “The pattern feels familiar,” he says. “In the late 1990s the internet was genuinely transformative, yet valuations priced in perfection and capital chased anything with a dot‑com suffix. Today, AI is genuinely transformative, valuations again price in perfection, and money chases anything with ‘AI’ in the pitch deck.”

Why AI looks different—and why it doesn’t

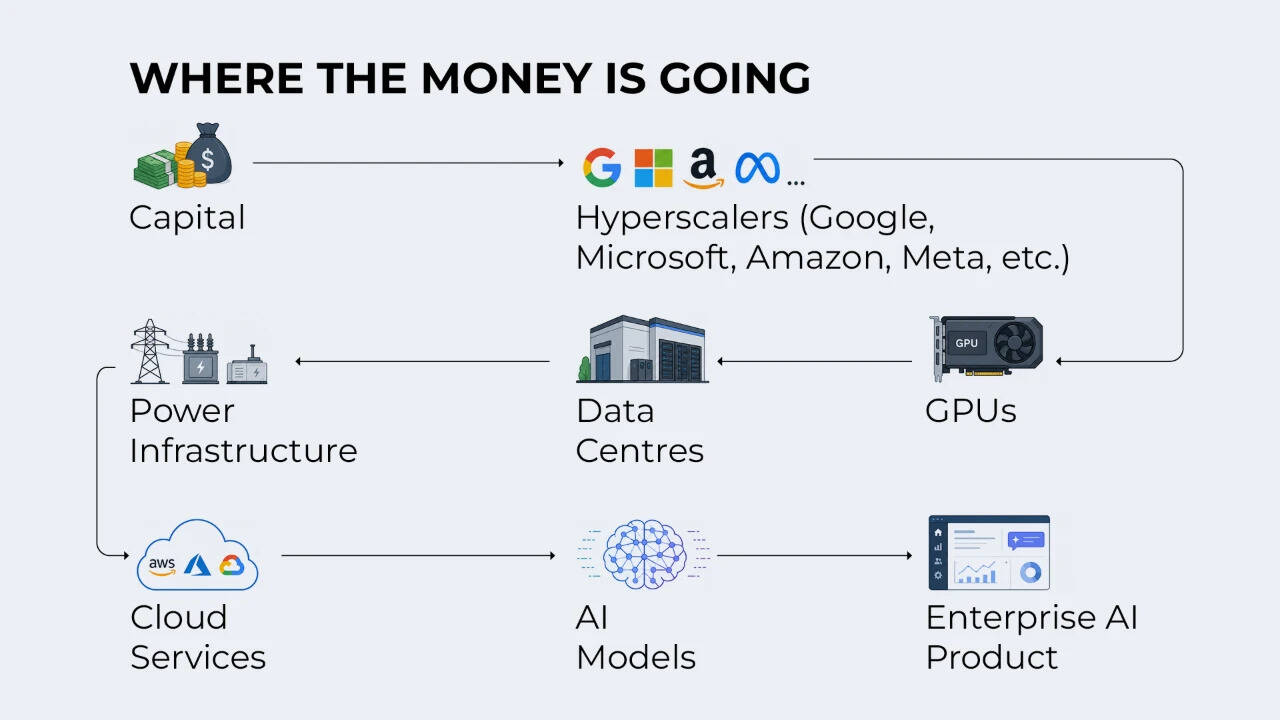

Unlike many internet start-ups of the dot-com era, today’s AI boom is being driven by some of the world’s largest and most profitable companies. Technology giants are funding unprecedented investments in data centres, advanced chips, cloud infrastructure and power-intensive computing facilities.According to the BIS, spending plans by leading hyperscale technology firms are expected to exceed one trillion dollars across 2025 and 2026. That level of capital expenditure is virtually unprecedented outside major public infrastructure programmes.The report recognises that generative AI could eventually lift productivity across industries, improve business efficiency and stimulate long-term economic growth. Yet it also highlights an important uncertainty: nobody knows when these investments will begin generating returns large enough to justify their extraordinary scale.Prashanth Kaddi, Partner and Leader, AI & Data and Engineering at Deloitte India, says Indian enterprises are increasingly embedding AI into their core operations. “According to our research, 40% of Indian respondents report significant or full AI usage, indicating that organisations are moving beyond pilots and operationalising AI to drive productivity and business outcomes.”

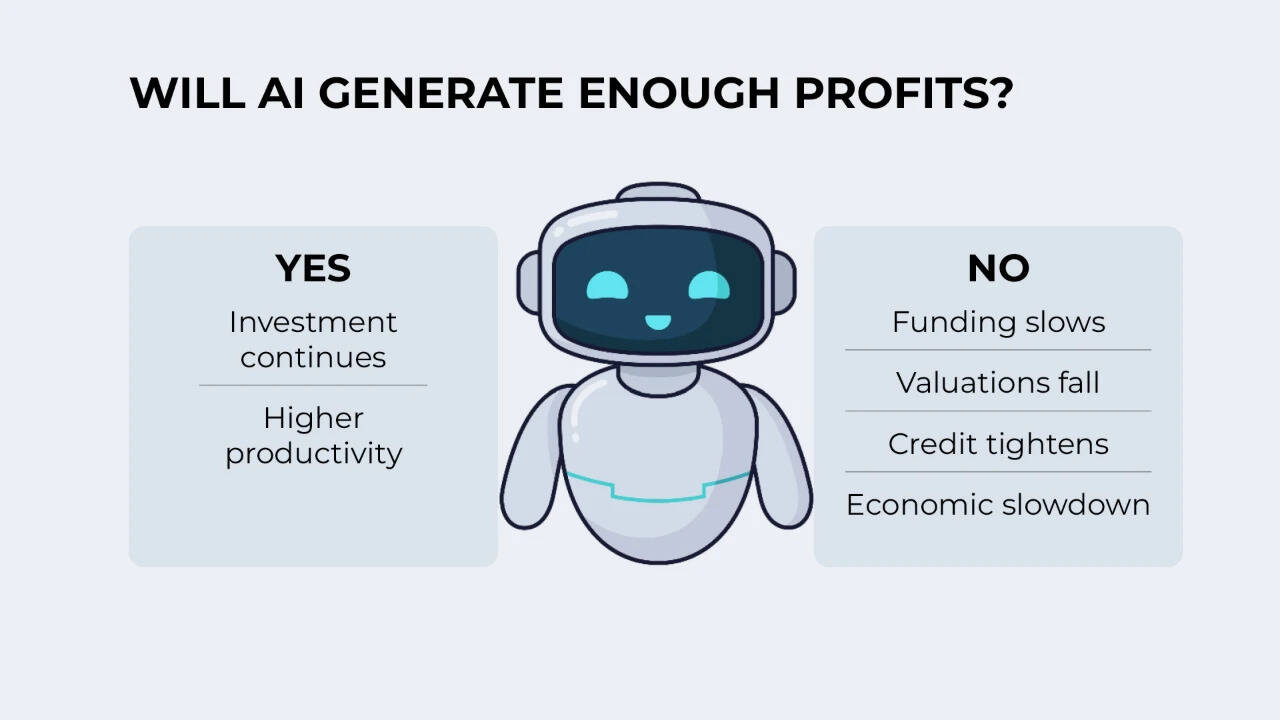

“The key question,” the BIS argues, is whether current investment can ultimately produce “sufficiently profitable applications.”That uncertainty matters because markets are already pricing in remarkable success.

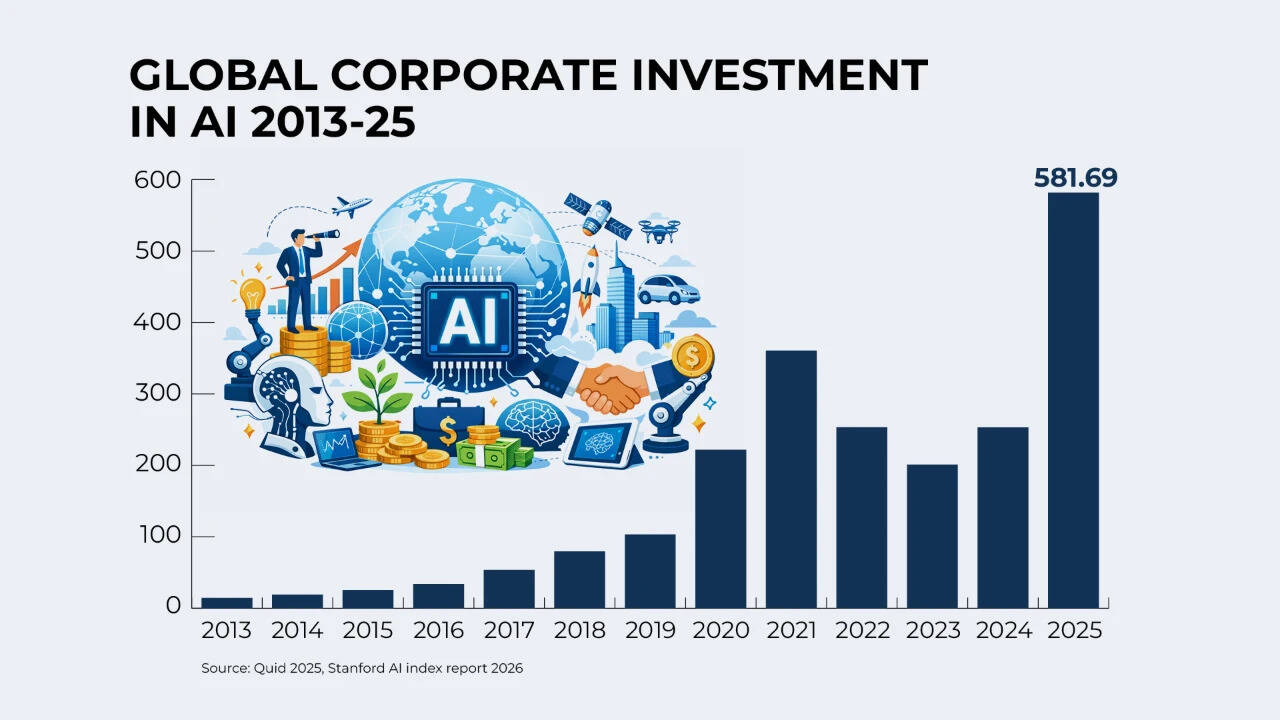

The global AI investment surge

According to the Stanford AI Index Report 2026, global corporate AI investment more than doubled in 2025, with private investment rising by 127.5% and generative AI funding growing by more than 200%. The United States alone attracted $285.9 billion in private AI investment, over 23 times China’s $12.4 billion, while AI computing capacity expanded at an estimated 3.3 times per year since 2022, reaching approximately 17.1 million H100-equivalent GPUs.In India, Reliance Industries announced a $109.8 billion commitment to AI infrastructure over seven years, contributing to a broader national ambition of investing more than $200 billion in AI infrastructure, a dramatic leap from the country’s cumulative private AI investment of approximately $11.1 billion between 2013 and 2024. Microsoft announced that it is on track to invest US$50 billion by the end of the decade to expand AI capabilities across countries in the Global South, building on its previously announced US$17.5 billion AI investment in India. Meanwhile, the Government of India announced a major expansion of the IndiaAI Compute Portal, adding more than 20,000 GPUs and increasing the country’s national AI compute capacity from approximately 38,000 GPUs.

The risks beneath the optimism

One of the BIS’s central concerns is not simply the amount of money flowing into AI but the way it is being financed.The report notes that AI investment has become increasingly concentrated among a relatively small group of firms that dominate computing infrastructure, semiconductor demand and cloud services. Such concentration can amplify financial vulnerabilities if expectations change abruptly.The BIS also points to the growing role of debt financing and private credit in supporting parts of the AI ecosystem. When borrowing rises rapidly alongside optimistic revenue expectations, financial systems become more vulnerable to disappointment.Yet, industry leaders caution against mistaking concerns over valuations for doubts about the technology itself. Amit Chaurasia, the Founder of Dataneers said, “One thing is clear – AI is NOT a hype. It is here to stay. How valuable – Let time pass by. When it comes to bubbles – let the investors and invested worry.”Kaddi says businesses are increasingly convinced of AI’s return on investment. “Our (Deloitte) research shows that 97% of organisations expect AI to improve productivity, reflecting strong confidence in its value creation potential. Organisations are no longer just experimenting with AI—they are embedding it into how they create value and compete.”

History offers plenty of examples.During investment booms, capital is often abundant because everyone assumes future demand will justify today’s spending. If revenues fall short, companies cut investment, lenders become cautious and asset prices adjust quickly.That does not necessarily mean AI is a bubble. It does mean that financial markets could face turbulence if expectations prove too optimistic.The Dataneera founder believes the AI investment wave also reflects a familiar tendency to chase prevailing trends. “In India, we often follow the herd,” he says. “In the 2000s, IT was booming, so every student wanted to pursue engineering in computer science. Today, we’re seeing a similar rush around data centres and GPUs. Governments across the country are actively promoting investments in data centres, but I’m not convinced these decisions are always backed by rigorous research or long-term strategic thinking.“The BIS therefore urges policymakers to monitor not just technological progress but also the financial structures developing around it.

This isn’t 1999

Despite the comparisons, equating AI with the dot-com bubble would oversimplify the situation.The internet economy of the late 1990s was dominated by thousands of relatively young firms with uncertain business models.Today’s AI race is led by companies generating billions of dollars in annual profits from cloud computing, software, advertising and enterprise technology. Their balance sheets are considerably stronger than those of most dot-com companies.Vishwa Kiran says the AI boom differs from previous technology cycles because it is driven by profitable companies generating real revenues, with adoption accelerating across consumers and enterprises alike. “Unlike the dot-com era, revenue exists from day one,” he says. However, he cautions that investment is “highly concentrated in a handful of companies.”Moreover, AI products are already generating measurable commercial value.Businesses are using AI to automate coding, customer support, data analysis, drug discovery, logistics, financial services and industrial design. Governments are deploying AI across public administration, while consumers increasingly rely on AI-powered search, writing tools and digital assistants.The question, therefore, is not whether AI has real-world applications. It clearly does.The uncertainty lies in whether current market expectations assume returns that are simply too optimistic, too broad or too immediate.History suggests transformative technologies often require longer periods before their economic benefits become fully visible than financial markets initially anticipate.

A different kind of financial risk

The BIS’s investment concerns arise as regulators grapple with another AI challenge: cybersecurity.The Reserve Bank of India’s Financial Stability Report (June 2026) echoes warnings from the BIS’s Annual Economic Report 2026. While the BIS says AI investment has underpinned global growth, it cautions that the trillion-dollar buildout of AI infrastructure, opaque financing arrangements and rising private credit exposure could threaten financial stability. Similarly, the RBI warns that debt‑funded AI investments and banks’ indirect exposure through private credit and other intermediaries could amplify systemic risk if AI-related valuations correct sharply.Unlike the BIS’s valuation concerns, these are operational risks rather than market‑pricing risks. Together, however, they underscore a broader reality.AI is reshaping finance in multiple ways at once — through investment flows, risk management, fraud detection, cybersecurity and financial stability.That means regulators must think beyond traditional market cycles.

What history teaches

Every major technological revolution has prompted bouts of exuberance.Railways transformed transport but sparked speculative manias. Electricity changed manufacturing and unleashed waves of financial speculation. The internet reshaped communication, even as countless internet companies collapsed.Artificial intelligence may become the defining technology of the twenty-first century. The BIS does not dispute that possibility; it cautions against assuming technological breakthroughs automatically produce proportionate financial returns.Markets often price tomorrow’s successes as if they have already arrived.Sometimes they are right.Sometimes those successes arrive years later than expected.Sometimes only a handful of firms ultimately justify the optimism that once surrounded an entire industry.

So, is AI heading for a dot-com moment?

The honest answer is: nobody knows.The BIS is not forecasting an imminent collapse. Rather, it is urging investors, policymakers and regulators to separate technological excitement from financial sustainability.Chaurasia says every transformative technology requires significant capital before it reaches mass adoption. “Earlier, it was the internet. Today, it is AI,” he says. “There will certainly be a churn as early investors seek returns on high-risk technology… some will burst and some will bloom. This is not a new phenomenon.”That distinction may prove crucial.AI could ultimately transform healthcare, education, manufacturing, finance and scientific research as profoundly as the internet transformed communication and commerce. But history suggests that even revolutionary technologies are not immune to periods of excessive enthusiasm, inflated valuations and painful corrections.The dot-com bubble was not evidence that the internet had failed. It was evidence that markets had become impatient.Yet there is one crucial difference. AI adoption has been unprecedented in both speed and scale. ChatGPT reached 100 million monthly users within two months of launch. Today, billions use AI-powered tools, from voice assistants to recommendation engines. By contrast, internet adoption in 2000 was far more gradual, with online usage and mainstream consumer applications still in their infancy.Kaddi believes AI remains a major engine of global investment despite macroeconomic uncertainty. “AI has been a key driver of growth despite geopolitical tensions and a challenging economic environment. Continued investments in data centres, chips and cloud infrastructure will have ipple effects across global supply chains, particularly in Asia, boosting demand for semiconductors, data storage hardware and related technologies.“The BIS’s warning is, in many ways, less about artificial intelligence than about human behaviour. Technologies change. Investor psychology does not.If the AI revolution fulfills even a fraction of its promise, today’s enormous investments may eventually look prescient rather than excessive.But until profits catch up with expectations, one question will continue to shadow the world’s biggest technology boom:Are we funding the future, or simply pricing it too far ahead of schedule?